Let's Just Hope Shipping

Isn't Telling the Real Story of China

December 9, 2015 — 7:00 PM ESTUpdated on December 10,

2015 — 9:12 AM EST

Shipping index falls

to record at time when it should rally

·

Coal, iron-ore imports

in first reversal for more than decade

Investors betting that China’s near-insatiable appetite for

industrial raw materials will drive global economic growth may want to skip the

shipping news.

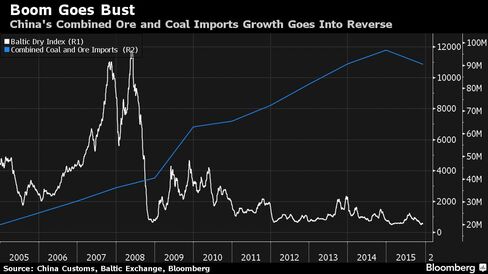

For the first time in at

least a decade, combined seaborne imports of iron ore and coal -- commodities

that helped fuel a manufacturing boom in the world’s second-largest economy --

are down from a year earlier. While demand next year may be a little better,

slower-than-anticipated growth in 2015 has led to almost perpetual

disappointment for shippers, after analysts’ predictions at the end of 2014 for

a rebound proved wrong.

The world has surpluses

of everything from corn to crude oil, and commodity prices are heading for

their biggest annual loss since the financial crisis. With China’s economy

expanding at the slowest pace since 1990 demand has ebbed from one of the

biggest importers. The Baltic Dry Index of shipping rates for bulk materials

fell to an all-time low last month, turning those who watch the industry

increasingly bearish.

“For dry bulk, China has

gone completely belly up,” said Erik Nikolai Stavseth, an analyst at Arctic

Securities ASA in Oslo, talking about ships that haul everything from coal to

iron ore to grain. “Present Chinese demand is insufficient to service dry-bulk

production, which is driving down rates and subsequently asset values as they

follow each other.”

Growth Reversal

China produces about half

the world’s steel. The metal is made from iron ore in furnaces fueled by coal,

which also is used to run power plants. While domestic mines supply both raw

materials, it isn’t enough, so the country must buy from overseas. As the

economy surged over the past decade, imports of iron ore tripled, and coal

purchases rose almost four-fold since 2008, government data show. The country

accounts for two in every three iron-ore cargoes in the world, and is the

largest importer of soybeans and rice.

But this year, demand has

slowed. Combined seaborne imports of iron ore and coal will drop 4.8 percent to

1.097 billion metric tons, the first decline since at least 2003, according to

data from Clarkson Plc, the biggest shipbroker. A year ago, Clarkson was

anticipating a 5.5 percent increase for 2015. The broker expects growth to

increase just 0.04 percent next year.

It may get worse. The

China Iron and Steel Association predicted crude-steel output will tumble by 23

million tons to 783 million tons next year. That lost output is more than a

quarter of what U.S. steelmakers produce.

The Baltic Dry Index

slumped to 504 points on Nov. 19, the lowest since 1985. It has subsequently

advanced to 534 points. While rates for iron ore-carrying Capesize ships

normally rise at the end of the year, owners are bracing for the weakest fourth

quarter since 2001, Baltic Exchange data show.

Estimates Revisited

At the end of last year,

shipping analysts forecast rates for Capesize-class vessels would jump by about

a third in 2015. Instead, they’re now expecting a decline of about that

magnitude.

Imports are weakening

even as China’s economy keeps expanding because of reduced spending by local

governments that are dominant players in the economy, according to Fielding

Chen, a Hong Kong-based economist for Bloomberg Intelligence. The central

government in January withdrew guarantees for Local Government Financing

Vehicles used to finance infrastructure projects during the country’s boom

years, when domestic capacity surged over the past decade, he said.

“This has reduced China’s

appetite for steel and copper and other commodities that are used to build

roads, subways and reservoirs,” Chen said. “It is not good for the economy and

is one of the main reasons China cannot import more.”

Glut of Ships

Economic growth, which is

still about half its pre-2008 peak, is also being propped up by increased

consumption and services, and a higher rate of spending by the central

government, he said.

Sliding Chinese demand is

just part of the reason for the slump in freight rates. There are also more

ships, and low scrap-steel prices have discouraged demolitions of older

vessels, according to Nigel Prentis, the head of consultancy at Hartland

Shipping Services Ltd. in London. The fleet will expand 4.1 percent next year

compared with an expansion in demand for dry-bulk commodities of 1.6 percent,

estimates Clarkson.

“A lot of people ordered

vessels believing in the continued growth in Chinese imports,” said Erik

Folkeson, an analyst at Swedbank First Securities in Oslo. “When that failed to

materialize, utilization level dipped. I struggle to see the big triggers for a

recovery.”

The Twilight Zone

The rout in buying showed

signs of easing last month. China’s iron-ore imports rose to 82.13 million

tons, a jump of 22 percent compared with a year earlier. Even so, the extra

shipments are mostly because of rising Chinese steel exports, rather than the

nation’s own demand, according to Andy Xie, an independent economist who

predicted in February that iron-ore prices would sink into the $30s this year,

compared with $71 at the start of the year.

Chinese steel mills have

been pressured by losses, low prices and overcapacity as demand drops to levels

unseen since 2009, cutting profits and reducing incentive for re-stocking.

“China’s slowdown has

come as a major shock to the system,” said Hartland Shipping’s Prentis. “We are

now caught in the twilight zone between shifts in China’s economy, and it is

uncomfortable as it’s causing unexpected slowing of demand.”

No comments:

Post a Comment