Here are some important questions for today's corporations: Can companies do well while doing good? Does a company that improves its social or environmental performance increase, decrease, or leave unchanged its financial performance?

These are the questions George Serafeim, an associate professor of business administration at the Harvard Business, has been trying to answer with some help from other academics. It is interesting work.

| |

| The Green Supply Chain Says: |

This research found that firms in the high sustainability group significantly outperformed firms in the low sustainability group in terms of both stock market performance and accounting measures. This research found that firms in the high sustainability group significantly outperformed firms in the low sustainability group in terms of both stock market performance and accounting measures. |

What Do You Say?

|

|

In a lengthy report on think tank Brooking Institute's web site, Serafeim notes the sea change in the last couple of decades in how the public and company executives view corporate behavior. Largely gone is the notion that company's should only focus on profits and stock prices. Now, there is pressure to do social and environmental good at the same time.

Serafeim notes, for example, that in the early 1990s, there were fewer than 30 companies producing a report relative to environmental or social activities. Twenty years later, more than 6,000 companies in the world produced such reports.

But he also notes that while in many cases sustainability initiatives, such as reducing energy consumption, will deliver benefits to the bottom line and society. But the link between many other sustainability efforts and profits and stock price are unclear at best, obviously to an extent reducing their attractiveness to executives.

The question becomes whether there is a net cost in financial terms from improving non-financial (social, environmental) performance. That could be the case, for example, in moving to cleaner but more expensive energy sources or increasing wages in offshore factories.

Serafeim, along with Ioannis Ioannou of the London Business School andRobert Eccles of Harvard Business School, did some research a couple of years ago, in which they took sets of very similar companies (180 in total), one of which was deemed to that have explicitly placed a high level of emphasis on employees, customers, products, the community, and the environment as part of its strategy and business model. Those companies were identified using as a template of business policies identified by corporate data research firm Thomson Reuters.

The three researchers then looked at financial performance across a number of measures from the early 1990s through 2010, needing some 20 years of data due to the belief that the payback from being socially responsible may often take some time to arrive. It also went back that far to identify firms that moved towards social and environmental sustainability before it became so in vogue as it is currently and avoid companies that really only adopted such policies as "window dressing."

"The long-term approach is consis¬tent with sustainability strategies enhancing the brand of a firm, raising employee morale, attracting better talent, gaining better access to finance, and securing a license to operate." Serafeim says. "All these effects are built slowly and require a continuous commitment by a firm."

The result was a classification of 90 firms as having "high sustainability" and another 90 characterized as "low sustainability." At high sustainability firms "the notion of "sustainability" appears to be embedded in a holistic and multidimensional manner within and throughout the organization."

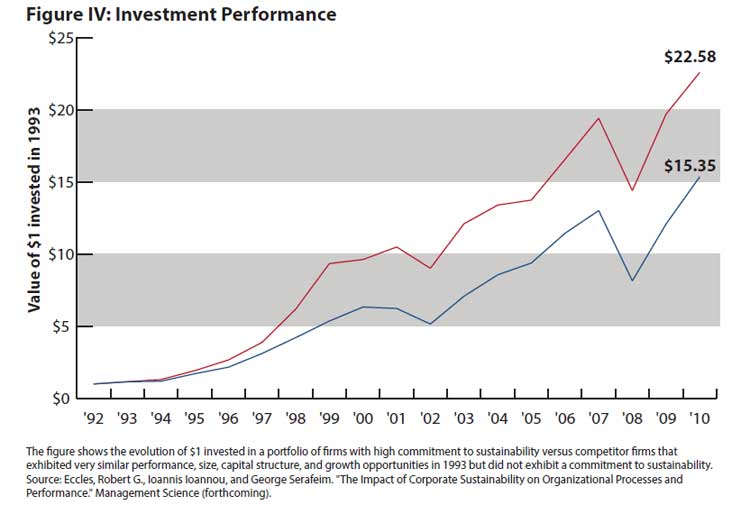

This research found that firms in the high sustainability group significantly outperformed firms in the low sustainability group in terms of both stock market performance and accounting measures. Investing $1 in the beginning of 1993 in a value-weighted portfolio of sustainable firms would have grown to $22 by the end of 2010 (red line in figure below). In contrast, investing $1 in the beginning of 1993 in a value-weighted portfolio of traditional firms would have only grown to $15 by the end of 2010 (blue line).

High Sustainability Companies Far Outperform Others in Stock Performance

On a risk-adjusted basis the outperformance was 4.8% annually.

The research found similar results for the measures of return-on-assets and return-on-equity. Moreover, this outperformance was more pronounced for companies that sell products to the end consumer (i.e., business-to-customer [B2C] companies), compete on the basis of brand and reputation, and make substantial use of natural resources. The report says this outperformance is "being driven by how those companies are managing their natural, human, and social capital."

"Multiple studies have now appeared that document similar benefits, showing how [high sustainability] companies benefit through better access to financing, customer satisfaction and loyalty, and better employee relations," Serafeim writes.

The key point, he adds, is that a firm's activities produce more than just products and services. "Externalities" are another outcome of a company's activities. Positive externalities arise when a company's actions generate marginal private benefit that is smaller than the marginal social benefit.

Serafeim notes, however, that firms have different "materialities" when it comes to how different forms of capital (e.g., human capital, natural resource capital, etc.) drive company and stock market success. There is on-going research to calculate those relationships for a given firm.

"This is no easy task, and in the last 3-4 years significant progress has been made in this domain," Serafeim notes. "An increasing number of companies are conducting stakeholder engagement exercises in order to identify the material issues and they are disclosing materiality matrices where they show the importance of different issues to the company and to society based on the perceptions of the company and their stakeholders respectively."

In conclusion, Serafeim writes that "While ten years ago most companies had sustainability programs that were inward focused, concentrating on cost savings, risk management, and downside risks, we are observing a new tendency to integrate sustainability at the core of the business, adopting an external orientation, identifying new needs and markets, and concentrating on value creation and upside potential."

The GreenSupplyChain notes there could perhaps be some other explanations for the increased valuation over time for high sustainability companies. For example, perhaps high profit firms have more latitude to pursue sustainability agendas, making high sustainability a result not a cause of outsized stock valuations.

Still, this is very excellent research that has been supported by other such studies as well, as Serafeim observed above.

|

No comments:

Post a Comment