Still fighting the omnichannel battle

The pressing need to learn how to handle omnichannel fulfillment profitably is reshaping retailers' supply chain strategies, according to preliminary results of the 2017 "State of the Retail Supply Chain" study.

By Toby Gooley

FIRST THE GOOD NEWS: U.S. holiday retail sales in 2016 were up more than 4 percent over sales during the same period in 2015. Now the bad news: That didn't seem to help retailers much. In December and January, several major chains announced or carried out layoffs and store closings, including Macy's, JC Penney, CVS, and The Limited (the last of which recently closed all of its mall stores). This comes on top of the 2016 demise of Sports Authority and store closing announcements by Sears, Kmart, Ralph Lauren, Office Depot, and others. Even Walmart is closing hundreds of stores.

The economic, technological, and societal forces that have converged to create this industrywide upheaval are many and complex. Online shopping, changing consumer preferences, the explosive growth in the number of e-commerce competitors, the cost and operational challenges of omnichannel operations ... those are just a few of the factors affecting retailers' ability to survive and remain profitable. Some of the responsibility for minimizing or counteracting the resulting damage falls on the shoulders of supply chain managers. That is likely why respondents to the Retail Industry Leaders Association's (RILA) 7th annual "State of the Retail Supply Chain" survey said controlling supply chain costs would be their top strategic priority in 2017.

The difference from year to year is striking. In 2016, "enhance customer service" was the top strategic priority, cited by 30 percent of respondents as their primary concern. This year, just 8 percent said that would be their primary focus in 2017. Instead, 42 percent of respondents said controlling supply chain costs would be their main strategic priority, up from 28 percent last year. Supporting revenue growth was second, with 31 percent (up from 22 percent in 2016), while balancing cost and service was third, at 19 percent, the same as last year.

For the latest survey, professors Brian Gibson, Rafay Ishfaq, and Cliff Defee of Auburn University's Harbert College of Business polled RILA's members, DC Velocity's readers, and retailers that collaborate with the Auburn, Ala., university's Center for Supply Chain Innovation. To round out the picture, the research team conducted telephone interviews with retail supply chain executives. The study's final results will be released at RILA's 2017 Retail Supply Chain Conference in Orlando, Fla., in mid-February, but the preliminary findings discussed in this article provide useful insight into how retailers are managing their supply chains in an increasingly omnichannel world.

THREE HOT TOPICS

The survey's 60 or so respondents represent U.S. retailers of all sizes, with projected 2017 revenues ranging from below $1 billion to more than $10 billion. They are also well qualified to speak about supply chain strategy: About 33 percent hold director or vice president positions, and 50 percent classified themselves as managers. Respondents have 20 years of supply chain management experience on average.

Each year, the study zeroes in on three "hot topics." This year, those topics were cross-channel integration, analytics, and cost control and recovery. All three are critically important at a time when retailers must be able to track, manage, and deploy inventory across an enterprise, regardless of location or sales channel, while responding to&mdashand often anticipating&mdashcustomers' preferences. Those mandates no doubt inform respondents' plans for supply chain-related investments in 2017. Compared with 2016 spending levels, 43 percent plan to increase their investments in supply chain process improvements, 37 percent plan to expand their omnichannel fulfillment capabilities, and 36 percent said they plan to upgrade their supply chain technology and software.

Here are some highlights from the preliminary survey results as well as a sampling of the researchers' comments on those findings:

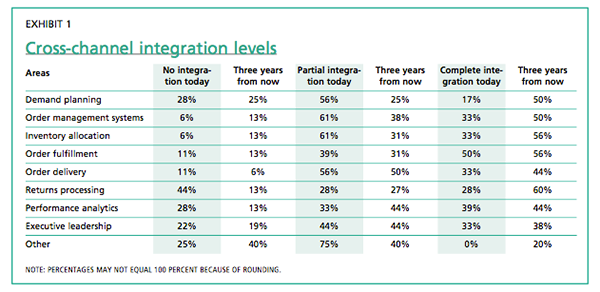

- Cross-channel integration. The survey asked about supply chain integration in the context of omnichannel retail. Just over a third of respondents said they are pursuing integration of online and store fulfillment activities, while 16 percent said they had already achieved that goal. Not everyone believes such integration is necessary, though: 24 percent said they would continue to keep online and store fulfillment separate.

As for the degree of cross-channel integration achieved to date, respondents counted themselves most successful when it came to order fulfillment, with 50 percent saying they've already achieved complete integration and 39 percent saying they have partially integrated that function. One-third said they have completely integrated order management systems, inventory allocation, and order delivery across channels. It's telling that 44 percent currently have no cross-channel integration in returns processing, a costly and complex activity that's proving to be a thorn in retailers' sides.

Why so much variation? "When people respond, they are drawing upon their area of expertise and how they see integration in their own functional areas," observes Ishfaq, an assistant professor and research fellow in supply chain management at the school. "Somebody on the warehousing side will have a different perspective than someone on the merchandise side."

Respondents have ambitious goals for the future. When asked what level of integration they expect to achieve three years from now, 50 percent or more said they would achieve complete integration in demand planning, order management systems, inventory allocation, and order fulfillment. Interestingly, 60 percent said the same for returns management, signaling that this area will be getting a lot more attention than it has in the past. (See Exhibit 1 for a "now" and "three years from now" comparison.)

None of that will be easy to achieve, cautions Gibson, who is a professor of supply chain management at Auburn and the study's leader. He calls the level of integration required for effective omnichannel operations "mind-boggling." The detailed work of implementation and obtaining visibility over inventory across channels is challenging, and groups that traditionally did not communicate much, such as supply chain and merchandising or store operations, must now collaborate very closely, he explains. Furthermore, retailers' approach to incentives and rewards can discourage decision-makers from taking a hit for the team, that is, taking on additional costs that may make their function's performance look subpar but will benefit the overall organization. Still, he adds, "the level of omnichannel integration compared to where we were when we first started the survey has vastly improved."

- Analytics. Respondents clearly see value in supply chain analytics, ranking "improving forecast accuracy" and "retaining current customers and sales" as the top benefits of developing such capabilities. Next on their list was "capture new customers and sales." It's notable that customer- and sales-related benefits ranked higher than such obviously supply chain-related benefits as optimizing inventory investments and improving order fill rates. That may reflect the influence of lessons learned from last year's strategic focus on customer service.

Very few respondents consider their organizations to have advanced capabilities when it comes to the use of the four types of supply chain analytics: predictive (which are designed to project what will happen in the future), prescriptive (to establish forward-looking strategies and capabilities), descriptive (to evaluate current conditions), and diagnostic (to understand why results occurred). The majority said they have either "basic" or "intermediate" capability, while in each of the four categories, a little more than one-fourth said they have no capability at all. The areas where respondents currently make the most extensive use of analytics are inventory planning and allocation, and customer needs analysis. Only 18 percent said they use analytics extensively in their returns operations, an area many retailers are struggling to manage.

Respondents were on the same page when it came to their assessment of what it takes to develop analytics capabilities. Ninety percent either agreed or strongly agreed that having an enterprisewide strategy is critical to success. Similarly, 86 percent agreed that effectively managing the volume and complexity of supply chain data is a major success factor, and 80 percent said the same about sharing data and analysis with supply chain partners. Three other high-ranking factors highlighted the human side of analytics: investing in analytics tools and talent (86 percent), executives understanding the benefits and limitations of analytics (85 percent), and hiring individuals with both supply chain and analytics expertise (80 percent).

The human factor should not be underestimated. "Almost everybody we spoke to said they have a big issue with finding the right talent," Ishfaq says. "It's one thing to purchase software, but you need people to work the data you collect into actionable information. This is one of the underlying challenges that is a temporary impedance to the extensive use of business analytics across the supply chain."

- Cost control and recovery. Currently, 50 percent of respondents partially recover the costs of providing omnichannel fulfillment and delivery services, and another 40 percent of respondents recover none of those costs. Ten percent do not even measure omnichannel cost recovery. In fact, only 40 percent of respondents believe it's even possible to fully recover those costs—something no respondent has yet achieved. Furthermore, 95 percent of respondents said they expect the cost of their supply chain operations to increase in the near future, which could push the cost-recovery goal further out of reach.

In a bid to at least partially recover costs, many respondents are imposing service fees or plan to do so in the future. For example, two-thirds currently charge for expedited service, and one-third impose delivery fees for small orders. Other types of fees are far less popular, and 50 percent or more said they have no plans to collect fees for in-store fulfillment, returns shipments and processing, or small orders. (Some respondents may have selected "no intention to use" because the scenario does not apply to their business.)

Respondents were also asked to name the three most effective ways they could "monetize" or control retail supply chain costs. At the top of their weighted list was leveraging a single inventory pool across all channels, followed by encouraging customers to buy online and pick up orders in stores, having vendors directly fulfill orders, and charging delivery fees for all orders.

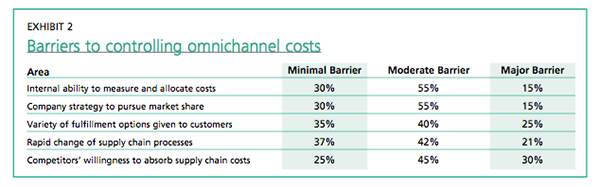

But there are significant barriers to implementing cost-control steps, including an inability to measure and allocate costs, the variety of fulfillment options offered to customers, and competitors' willingness to absorb supply chain costs. At least 60 percent of respondents considered each of the situations cited to be either moderate or major barriers to controlling omnichannel costs. (See Exhibit 2.)

Nevertheless, Gibson sees reason for optimism. Retailers are gaining a great deal of confidence in using analytics, and most understand the value of cross-channel integration, he says. But most supply chain organizations, he says, will struggle with omnichannel's biggest question: "How do we offset rising costs and make sure that as we take on additional supply chain costs, we're also driving revenue and profits? If you can answer that, you'll be in good shape," Gibson says. "If you can't answer that question, then you're going to be the next Limited or Sports Authority."

No comments:

Post a Comment