Productivity sags at top global ports

Turloch Mooney, Senior Editor, Global Ports | Sep 26, 2016 8:25AM EDTPrint

East and Southeast Asia, home to many of the world's largest ports, showed little improvement in productivity from 2014 to 2016.

East and Southeast Asia, home to many of the world's largest ports, showed little improvement in productivity from 2014 to 2016.

Productivity levels at the world’s top 30 container ports have shown little sign of improvement over the past two years, and ports in several world regions are showing worrying levels of decline, according to new analysis of port call and ship-tracking data by IHS Markit.

Port call data supplied by 74 percent of the world’s cellular fleet operators, combined for the first time with ship tracking satellite data, indicates that port productivity among the top 30 ports increased by just 2 percent between the first half of 2014 and the same period of 2016.

“With the exception of a few bright spots, the picture is not a good one,” said Andy Lane, partner with CTI Consultancy, who carried out the analysis on the data.

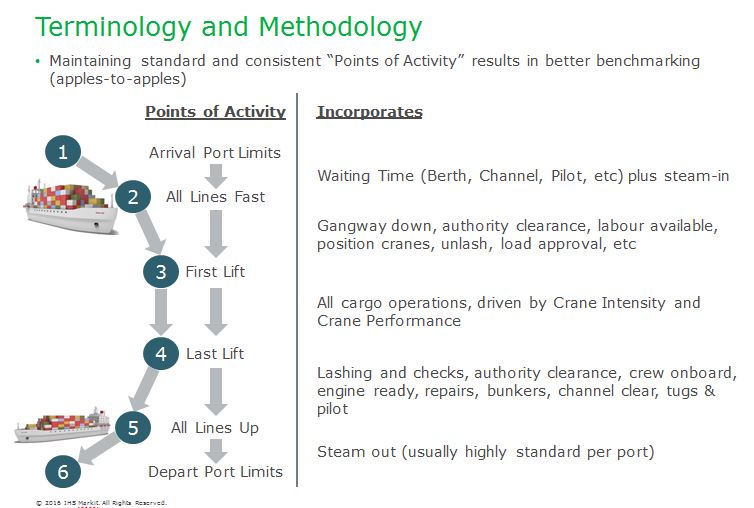

Port productivity is defined as the number of container moves per port call divided by the total hours from when vessels arrive at port limits to the point of departure from the berth.

Major ports in the Mediterranean booked the biggest decline in productivity as the combination of an increase in average steam-in time from 4.2 hours to 8.3 hours, and a 12 percent decline in berth productivity resulted in a 30 percent overall decline in port productivity.

{kind=link}

Among the largest ports in Southeast Asia, berth productivity improved by 6 percent but the gain was eroded by an increase in average steam-in time from 5.6 hours to 7.5 hours, resulting in a 3 percent decline in overall port efficiency.

“Most of the declines were experienced in 2015. We saw a slight rebound in the first half of 2016 but it was not enough to significantly impact the longer-term picture,” said Lane.

Major ports in some world regions showed an improvement in productivity. In North America, a reduction in average steam-in times by 2.1 hours offset a 13 percent decline in berth productivity to result in a 39 percent improvement in overall productivity; and large ports in North Europe experienced port productivity rise by 17 percent as average steam-in time also fell by two hours.

“Turning ships through ports and berths faster is win-win-win,” said Lane. “Ships with more sea time can steam slower to conserve fuel and reduce emissions, and they are more likely to arrive on time at destination. For the terminals, faster turnaround creates additional capacity without capex investment and therefore the potential to increase unit EBIT [earnings before interest and tax].”

Average wait times — calculated by subtracting standard steam-in time from overall port-to-berth time — improved in Africa, North Europe, and Oceania but declined in East and Southeast Asia, the Mediterranean, and Latin America, the data show.

Relative berth productivity, or RBT — calculated by dividing the number of moves by time at berth and weighted for average call-size — declined in most world regions between the first half of 2014 and the first half of 2016. Large ports in the Middle East, the Mediterranean, North America, and North Europe experienced RBT fall by 10 percent, 10 percent, 13 percent, and 1 percent, respectively, during the period. Slight improvements were booked in Southeast Asia and East Asia.

Despite the rationalization of networks by alliances, including reductions in the number of port calls, average call size for all vessels and classes remained largely static. Call sizes averaged 1,069 moves in the first half of 2014 and 1,077 moves in the first half of 2016.

Among the top 30 ports, average call size for vessels larger than 10,000 twenty-foot-equivalent units has risen to 2,430 from 2,344, the data show.

More than half of all calls involve handling of fewer than 1,000 moves and the quantity of calls that require more than 3,000 moves remains below 10 percent.

“We are experiencing only modest growth here, and 2,500 moves per port call should not be an issue to contemporary terminals,” said Lane.

No comments:

Post a Comment